INCOME TAX

An individual whose annual income is more than the basic exemption limit of ₹2.5 lakh is required to file an ITR. The basic exemption limit for senior citizens (60 years onwards and less than 80 years) is ₹3 lakh, and for super senior citizens is ₹5 lakh.

A company, a partnership firm or a LLP ITR filing is mandatory even if:

- No income

- Loss incurred

- No business activity

ITR filing is compulsory irrespective of income if any of the following applies:

- Deposited ₹1 crore+ in current account

- Spent ₹2 lakh+ on foreign travel

- Electricity bill ₹1 lakh+

- TDS/TCS deducted in your PAN

- You hold foreign assets or foreign income.

Yes, if you want to carry forward losses for the succeeding tax years.

If you incurred loss in:

- Business / profession

- Share trading (intraday, F&O)

- Capital loss (shares, mutual funds, property)

👉 ITR must be filed within due date to carry forward losses to future years for set-off.

⚠️ If you don’t file ITR → loss lapses forever.

An assessee is required to file an Income Tax Return once their annual income exceeds ₹2.5 lakh. The fact that TDS has been deducted by the employer does not eliminate the need for filing the return. At the time of filing, details of total income, eligible deductions, and TDS credit must be correctly reported.

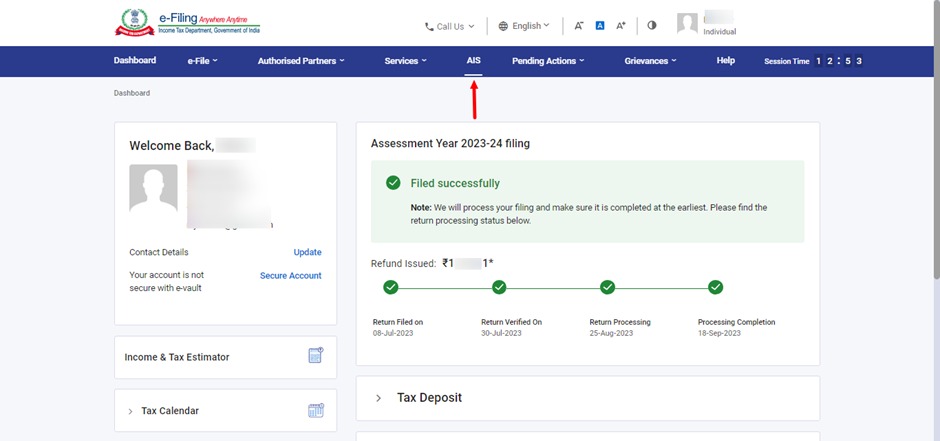

1. Check AIS (Annual Information Statement)

AIS shows almost all financial transactions reported against your PAN.

Steps:

- Log in to the Income Tax e-Filing Portal

- Go to Annual Information Statement (AIS) tab

- Review:

- Bank interest

- Mutual fund transactions

- Share trading

- Dividend income

- Property transactions

- TDS/TCS details

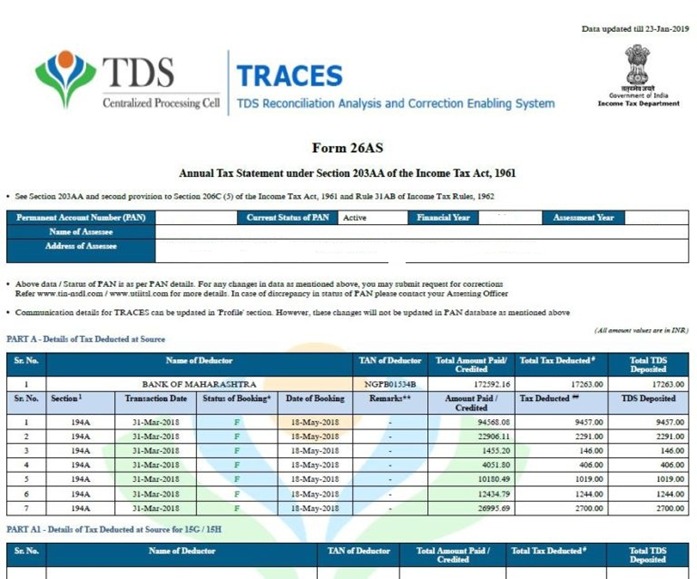

2. Form 26AS

Shows TDS/TCS and high-value transactions.

Check for:

- Bank FD interest TDS

- Dividend TDS

- Rent TDS (if any)

- Professional fees TDS

- 31st July – Most individual taxpayers (ITR-1 & ITR-2)

- 31st August – ITR-3 & ITR-4 (not required audit)

- 31st October – Companies & audit cases

Belated / Late Filing Due Date

If you miss the original due date, you can still file a belated return up to:

📍 31st December

But note:

- Late filing may attract a late fee and interest under the Income-tax Act.

- Some deductions or benefits could be restricted like carry forward of losses will not be allowed etc.

Revised Return (under Section 139(5))

Budget 2026 and tax authorities have introduced changes to revise timelines:

👉 You can file a revised return for FY 2025-26 up to: 📍 31st March (extended from earlier December 31)

A nominal fee may apply if the revised return is filed after December 31.

Verifying your ITR is mandatory—without verification, your return is treated as invalid. You must verify your ITR within 30 days of e-filing.

Instant verification: Aadhaar OTP (most popular)

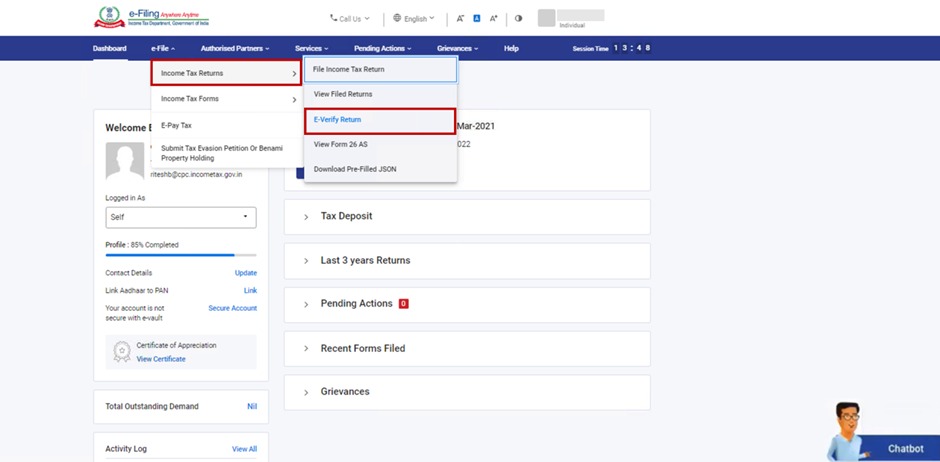

- Log in to the Income Tax e-Filing Portal

- Go to e-File → Income Tax Returns → Pending for e-Verification

- Select Verify via Aadhaar OTP

- OTP comes to your Aadhaar-linked mobile

- Enter OTP → Done.

Instant verification: if Aadhaar not linked then Net Banking

- Log in through your bank’s net banking

- Select Login to Income Tax Portal

- Go to e-Verify Return

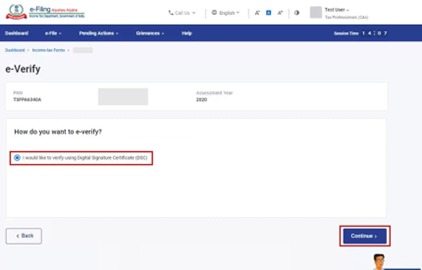

Instant verification: Digital Signature Certificate (DSC)

- Mandatory for Companies & LLPs

- Optional for others

- Attach DSC → e-Verify

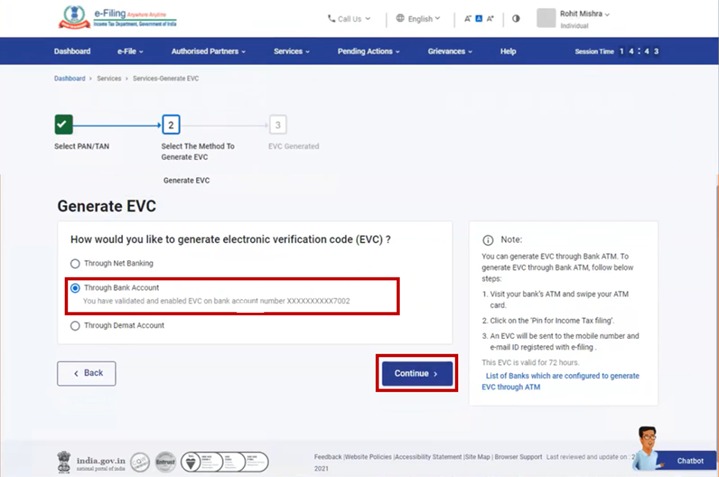

Instant verification: Bank Account / Demat Account (EVC)

- Generate EVC (Electronic Verification Code)

- Enter EVC on portal

- Bank/Demat must be pre-validated

Offline method (slower)

Send ITR-V by post

- Download ITR-V (Acknowledgement)

- Print & sign (blue ink)

- Send to: CPC, Income Tax Department, Bengaluru – 560500

- Must reach within 30 days

Important tips

- Filed but not verified = invalid return

- Refund processing starts only after verification

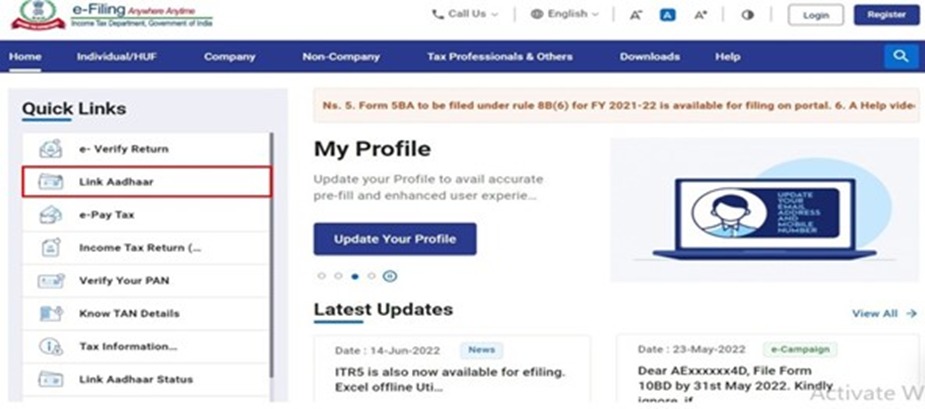

No worries—linking PAN with Aadhaar is simple and fully online.

- Visit the Income Tax e-Filing Portal

- Click Link Aadhaar (on homepage)

- Enter: PAN, Aadhaar Number, Name as per Aadhaar

- If Aadhaar not yet validated → OTP will be sent to Aadhaar-linked mobile.

- Enter OTP and submit

- You’ll see “PAN successfully linked with Aadhaar”

Aadhaar–PAN linking fee (important)

- If not linked within the original due date → ₹1,000 late fee

- Pay challan online (minor head 500) before linking

- After payment → proceed with linking

Common problems & solutions

- Name / DOB mismatch: Update details in Aadhaar or PAN first, then retry linking

- Aadhaar mobile number not active: Update mobile number at Aadhaar centre (OTP is mandatory)

- PAN already inoperative: Pay late fee, link Aadhaar, PAN becomes operative again automatically

Importance of Selecting the Correct ITR Form

- Prevents defective return notices

- Ensures smooth processing & refunds

- Avoids penalties and compliance issues

1. ITR-1 (SAHAJ)

Applicable to: Resident individuals, Total income up to ₹50 lakh, Income from: Salary / Pension, One house property, Other sources (interest, dividend, etc.)

Not applicable if: Capital gains income, Business or professional income, More than one house property, Foreign income or assets.

2. ITR-2

Applicable to: Individuals and HUFs, No business or professional income, Income may include: Salary / pension, Multiple house properties, Capital gains (shares, mutual funds, property), Foreign income / assets

3. ITR-3

Applicable to: Individuals and HUFs having: Business income, Professional income, Income from partnership firm (as partner). Includes: F&O trading, Intraday trading, Freelancing / consultancy, Proprietorship business

4. ITR-4 (SUGAM)

Applicable to: Individuals, HUFs, and Firms (excluding LLPs), Income computed under presumptive taxation: Section 44AD (business), Section 44ADA (profession), Section 44AE (transport business)

5. ITR-5

Applicable to: Partnership Firms, LLPs, AOPs / BOIs, Trusts (not filing ITR-7)

6. ITR-6

Applicable to: Companies (other than those claiming exemption under section 11). Filed mandatorily using Digital Signature Certificate (DSC).

7. ITR-7

Applicable to: Persons required to file returns under: Sections 139(4A) – Charitable trusts, 139(4B) – Political parties, 139(4C) / 139(4D) – Institutions, universities, colleges.

GST

1. Based on Turnover

- ₹40 lakh – Supply of goods (normal states)

- ₹20 lakh – Supply of services

- ₹20 lakh / ₹10 lakh – For special category states (NE & hill states)

👉 Turnover includes taxable + exempt + export + inter-state supplies (PAN-based).

2. Inter-State Supply

If you make inter-state taxable supplies, GST registration is compulsory irrespective of turnover.

3. E-commerce Related

- Sellers supplying through Amazon, Flipkart, Meesho, etc.

- E-commerce operators collecting TCS

👉 Registration compulsory, no threshold benefit.

4. Casual & Non-Resident Taxable Persons

- Temporary business in exhibitions/fairs

- Foreign entities supplying in India

👉 Registration required before starting business.

5. Reverse Charge Mechanism (RCM)

If you are liable to pay GST under RCM, registration is mandatory.

6. Agents & Special Categories

- Agents supplying on behalf of others

- Input Service Distributors (ISD)

- Persons required to deduct TDS/TCS under GST

- Online service providers (OIDAR)

7. Voluntary Registration

Even if not liable, you can opt for voluntary GST registration to: Claim Input Tax Credit (ITC), Do business with large corporates, Build credibility

Yes. Once you have voluntarily taken GST registration, you are fully liable to charge GST on your outward supplies, even if your turnover is below the threshold limit.

Yes, you need a separate GST registration (GSTIN) in the other state if you want to do business there, even temporarily.

Under Section 25 of the CGST Act, GST registration is state-wise. So:

GSTIN in State A ❌ cannot be used for supplying goods/services from State B.

You are treated as a Casual Taxable Person (CTP). Examples: Exhibition / trade fair, Temporary site work, Short-term consultancy / services, Seasonal business.

🔸 Registration is mandatory before starting business

🔸 Advance tax payment required (estimated liability)

Step 1 – Output GST

GST charged on sales. Example: Taxable sales ₹5,00,000 × 18% = ₹90,000

Step 2 – Input Tax Credit

GST paid on purchases. Example: Purchases ₹2,00,000 with GST ₹36,000 = Eligible ITC ₹36,000

Step 3 – Net Liability

Output GST – ITC = ₹90,000 – ₹36,000 = ₹54,000

Under Section 16 & Section 17(1) of the CGST Act: ITC is allowed only for goods or services used in the course or furtherance of business.

If the goods are for personal use, ITC is expressly blocked. Even if invoice is in firm’s name, GSTIN mentioned, payment from business account — ❌ ITC not admissible.

Examples of NOT Allowed ITC: Mobile phone for personal use, Household furniture, Personal clothing, Car for personal use, Personal travel/hotel stay.

Regular GST Taxpayer: GSTR-1 (12/year), GSTR-3B (12/year), GSTR-9 (1/year)

QRMP Scheme (Turnover ≤ ₹5 Crore): GSTR-1 (12), GSTR-3B (4), GSTR-9 (1)

Composition Scheme: CMP-08 (4), GSTR-4 (1)

Yes, even if there is no business, NIL returns are compulsory.

Monthly Filers: 11th of next month

Quarterly Filers (QRMP): 13th of month following quarter

Monthly Filers: 20th of next month

QRMP (Quarterly): Category X states: 22nd, Category Y states: 24th

Monthly Tax Payment under QRMP: PMT-06 by 25th of next month

You can revive (restore) your cancelled GST registration if:

- Cancellation was done by GST department (officer)

- Cancellation was due to non-filing of returns or non-compliance

- You are otherwise eligible to be registered under GST

📌 This process is called Revocation of Cancellation.

No expiry. GSTIN remains valid for a lifetime until you apply for cancellation or department cancels it due to non-compliance.

Yes — a registered person can apply for cancellation of GSTIN.

NO — a GSTIN itself cannot be transferred to another person or even to a family member.

GST registration is PAN-based. GSTIN is issued to a specific legal person. Another person (even spouse / son / brother) has a different PAN. Hence, GSTIN is non-transferable.